Cost Control for the Project Manager

1. INTRODUCTION

Good cost control is the hallmark of successful Project Managers. How do you do it? If it were easy, everyone would do it well. Well, it’s not easy and the bigger the project, the harder it is to do well. Controlling costs is basically the same whether the project is cost reimbursable or lump sum. The difference is whose money is at risk – the Owner’s or the Contractor’s.

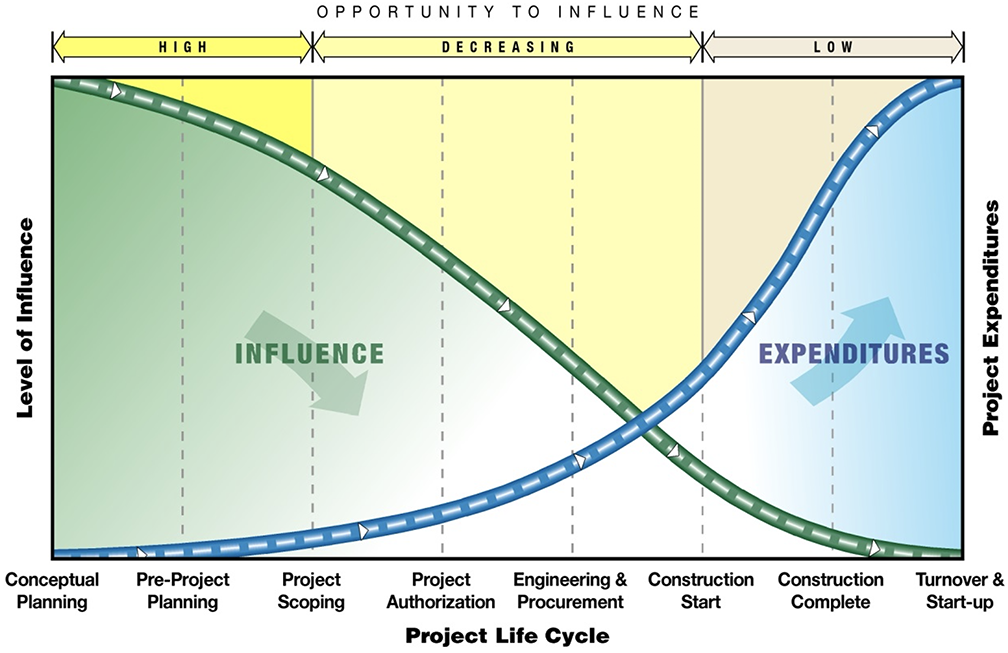

The first principle of cost is that every project has an ultimate cost. It can be minimized by clever execution or by removing unneeded scope and features, but there is an ultimate cost. The trick is first to estimate that cost early and then manage to it. Everyone has seen this cost influence curve:

Figure 1

Opportunity to Influence Project Expenditures in Construction

This curve, which has been extensively documented, demonstrates that the cost of a project can most be influenced at the start, during scope definition. As the project proceeds, the ability to influence the final cost decreases so that by the time detailed engineering and procurement are underway, the ability to influence the cost is in rapid decline and by the time engineering is complete and construction is underway, the ability to influence the project cost is very low.

The second principle of cost is that small things can have large effects. It’s relatively easy to keep track of the cost of the large elements – major equipment for example. It is quite another to keep track of small things – electrical cable, pipe fittings, or conduit fittings for example. Designing, procuring and installing the “little things” (called bulk materials in the process plant industry) can cost up to 60% of the total project costs. A 10% overrun across the board in bulks could result in up to a 6% increase in overall project costs. Even the practice of over-buying to create an “available surplus” of, say 10%, can increase the overall cost by 2–3%. The little things can really add up.

2. COST CONTROL DEFINITIONS

Here are the basic definitions of cost control:

- Deviation – any change from the current plan, whether or not it has cost, schedule, or quality implications. Deviations can be mitigated so that there is no impact on cost, schedule, or quality or they can become Trends or Change Orders.

- Trend – a Deviation that has been identified to have cost, schedule, or quality implications. On Cost Reimbursable contracts, trends are increases in the cost or extensions to the schedule of the project and are formally transmitted to the Owner. On Lump Sum projects, trends that do not become change orders are an additional cost to the Contractor and decrease his profit on the project.

- Scope Change – a Deviation that includes a change in project scope from the contractual basis.

- Change Order – a Trend or Scope Change that has cost, schedule, or quality implications and that changes the contractual basis for the project – extending the schedule, increasing the base cost, or changing the delivered project. Change Orders are normally formally signed off by both the Contractor and the Owner.

3. ESTIMATING

It is beyond the scope of this article to describe the art of estimating in any detail. Nevertheless, a good estimate (not fat and not un-creditably low) is the key to successful project execution. Knowing how to get a good estimate can be the secret to a good project.

It is often said “There aren’t any good estimators anymore. They all retired/quit/got promoted.” That cannot be true. Projects today are more complex, have more participants and, in some cases, are larger. Good estimates keep getting produced. Companies have developed cost databases that can provide historical cost information from which to complete the estimate. The trick is knowing what is in the database and how to apply it. Here, a good estimator is worth his weight in gold, but a good Project Manager working closely with estimating can accomplish the same result.

The Project Manager must deeply involve himself in the estimating process. That doesn’t mean doing the estimate (except perhaps for a small project), it means being involved in every decision, checking the scope that is being estimated, and testing the estimate using rules of thumb.

Above all else, the Project Manager must be the ultimate manager of the scope of an estimate. Deciding and documenting what is to be included in the estimate can save a lot of heartache and rework later. In creating the estimate scope, a lot of the uncertainties in the project will surface and can, hopefully, be resolved (or at least an allowance or contingency can be added). It’s easy to let the estimators work up the estimate with the engineers, procurement people, and construction staff, but by not involving himself in the day-to-day decision making, the Project Manager risks getting an estimate that does not really represent the project or (often) is high and no one knows why.

Once the estimate has been prepared and has undergone the normal checking, the Project Manager (and often his management) needs to review the estimate thoroughly. The first level of review should be with the engineers and others who created the estimate input. Check that the correct scope was used, that no additional contingency was added during this phase, and that every good cost saving idea has been developed and included. This is a good time to also check the man-hour estimates of engineering and other home office personnel. Some of the best reviews require each engineering and home office discipline to justify their man-hour estimates through discussing the scope that they will perform and comparing the project to historical norms for similar projects. These reviews typically are group sessions with all disciplines present to look for overlaps or gaps in scope between discipline groups or differences in approach. Spending half a day to several days on this detailed review is normally time well spent. By the end of the review, the Project Manager should have a firm grasp of the details of the estimate basis.

3.1 ESTIMATE TYPES

In the process industry, there are a number of different types of cost estimates. In many reimbursable projects, three estimates are made over the course of the project. Near the beginning of the project, estimators working with the process engineers, make an estimate based on the capacity of the process units and historical costs for similar units, adjusting the capacity by an appropriate factoring technique. This is referred to as a Capacity Factored Estimate and is often described as having ± 25% accuracy.

As greater design work is completed and pricing for major equipment is available, another estimate is prepared. This estimate, based on the major equipment and materials prices, uses historical relationships between the costs of major equipment and materials to arrive at the total project price and is referred to as a Materials and Equipment Factored Estimate and often has ± 10–15% accuracy.

Finally, there is the Definitive Estimate (also sometimes called a Detailed Estimate). This estimate is based on full details of the project – actual pricing of equipment and materials, detailed take offs of all materials, complete estimates of engineering and home office services, and detailed construction and staffing plans. Definitive estimates often are considered to have ± 5% accuracy.

4. EXECUTION PHASE

During the execution of the project, the Project Manager should take responsibility for the following elements of cost control in construction, with the assistance of the project management cost controls team:

- An overall project control plan that gives advance warning of undesirable trends, deviations, slippages and other project problems so as to facilitate timely corrective action to minimize the impact on project cost, schedule, and quality.

- The measurement and control tools including the automation plan to be used on the project.

- Obtain Owner approval, when required, for the control plan and tools to be used.

- Review and approve the project cost code of accounts and work breakdown structure.

- Ensure that exception reporting is implemented to keep project team members informed of deviations from the project execution plan.

- Ensure that cost trending and Change Order procedures are implemented early in the execution phase and that timely reports are available to involved project participants.

- Lead the preparation of and approve original project budgets and subsequent revisions.

- Ensure that cash flow forecasts are made and monitored.

- Lead the risk analysis to set project contingency.

- Control the use of project contingencies.

- Initiate and approve financial reports to the Owner and Contractor management (normally on a monthly basis).

5. COST OVERRUNS

Nearly all cost overruns originate from one of the following causes which are each described below:

- Poor Project Definition

- Poorly Drafted Contract

- Actions of the Owner

- Unrealistic Schedule

- High Cost of Home Office Services

- Overruns in Procurement and Subcontracting

- Construction Productivity

- Joint Venture Management

- Joint Venture Agreement

- Other Important Points

5.1 PROJECT DEFINITION

No one normally starts a project with the notion that the project is poorly defined. Poor Project Definition is often discovered later when comparing the “as built” scope to the “as estimated” scope. The Project Manager must conduct a thorough review of the project scope at the start and agree on it in detail with the Client. If the agreed scope is not what was estimated or priced in the contract, a Change Order must be prepared at the very start. It is amazing how often this step is overlooked in the excitement of project kickoff and how often, later, there is no agreement between the Owner and the Contractor about what the original scope of the contract was.

Another source of cost overrun in project definition is not having the basic process set (for a process plant). Many Owners ask the Contractor to provide “one each – process “X” plant.” The Process Plant can be supplied in a variety of ways and generally the Owner will have a lot of input. The Contractor who commits to providing “one each – process “X” plant” is at the Owner’s mercy and a very adversarial relationship is sure to ensue. Take the time, through Front End Loading, to define the plant thoroughly.

Another source of poor project definition is for project conditions and specifications to be unclear, inapplicable, or incomplete. Often Owner engineering organizations will specify that their (multi-volume) engineering specifications be used for a project when they may not apply directly or may need modification. Later, the Owner engineering organization may insist that changes to the specifications to make them applicable are at the Contractor’s expense or that the Contractor must conform, even though they don’t apply exactly.

The Project Manager must also watch out for subtle changes in conditions – geographic, climactic, seismic, or soil conditions. These may not have been sufficiently defined at the start of the project or may be discovered to be different from those specified in the contract. Likewise, administrative requirements of the Owner or a governmental agency may be quite different from what was anticipated at project start. Local labor rules, requirements for local content, and local vendors supplying materials may cause project costs to change. In particular, import regulations and taxes are often a source of cost “surprises” to the project and should be reviewed thoroughly at the start of the project and monitored constantly throughout the project for unanticipated differences.

5.2 CONTRACTS

Contracts are normally negotiated at the start of a project, often under severe time pressure. Not only can every eventuality not be anticipated at the start of the project, contract drafting defects can creep in. Contract clauses can be vague, ambiguous, or one-sided. Conditions for contract completion can be incomplete or unclear, particularly in the areas of transfer of care, custody, and control and start-up and performance tests. Warranties, how they are enforced, the dates and conditions for expiration of warranties, and the Contractor’s responsibilities for warranty “make good” are often neglected. Final contract close out including obtaining completion certificates, collections of reserves and retainage, conditions to be met in order to receive final payments, and release of bank bonds need to be drafted into the contract and monitored as to applicability at the end of the contract.

Agreements with potential subcontractors and other third parties are often not finalized at the effective date of the contract, creating potential for extra cost. The Project Manager must monitor subcontracting to be sure that subcontract Agreements have terms and conditions consistent with the prime contract and that there are no overlaps or gaps in the prime contract versus subcontracts.

5.3 OWNER

Actions the Owner takes can also cause cost overruns. Inexperienced Owner project team members (inexperienced in projects in general or with the specific project type) are often a cause of increased costs. Delays in Owner decisions or late modifications can also increase costs through reduced productivity and necessary rework. If the Owner’s preferred vendor and subcontractor list is too limited or if unsuitable suppliers are included, poor quality materials or higher costs for the materials may be incurred.

A project a number of years ago required the Owner have 15 calendar days to approve certain drawings. After that, if no comments had been received, the contract permitted the contractor to treat the drawings as Owner approved. Looking back, the Owner did submit comments on the drawings, but on the average, they took 25 days. In the meantime, the engineers and designers went on with their work and subsequently had to go back and incorporate the Owner’s comments (in order to keep peace with the Owner although the contractor was not contractually obligated to do so). In the end, the Owner’s tardy comments cost at least a month of overall schedule slippage and many millions of dollars in engineering and construction rework.Could project management have avoided this cost control problem? Probably – by taking a stand on comments and the time the Owner had to make them.

5.4 SCHEDULE

The importance of a 90-day schedule and a detailed execution schedule created at the very start of the project cannot be over emphasized. Costs can be increased either through unrealistic schedules being created or imposed (by management or by the Owner) or through not meeting the agreed schedule. Areas of poor schedule performance that can contribute to increased costs include:

- Late mobilization of personnel and resources both in the engineering office and the field;

- Decisions not being made at the time specified by the schedule;

- Performing activities out of sequence (Ex: mobilization of subcontractors too early);

- Late revision of documents considered finished;

- Delays in releasing purchase orders to vendors;

- Vendor drawings and data being issued late to the design team;

- Delays in issuing documents to the vendors and to the job site;

- Late deliveries of materials to the job site, in particular, bulk materials; and

- Cascading effects of delays of one discipline on another on the job site.

5.5 COST OF HOME OFFICE AND ENGINEERING SERVICES

Home office and engineering services costs can be overrun by a variety of causes, such as:

- Internal productivity problems caused by:

- Performing work out of sequence – resulting in increased costs from affected disciplines or rework

- Uncontrolled interfaces between disciplines

- Impact of changes by one discipline on the work of another;

- Late modifications and repetition of studies;

- Excessive management reports and documents;

- Excessive costs for computers and information technology; and

- Underestimating the man-hours required for job site support.

5.6 PROCUREMENT AND SUBCONTRACTING

Even the best procurement and subcontracting plans can run into cost difficulties. The market conditions for purchasing and subcontracting can be different from those anticipated during estimating with inflation or lack of qualified and available suppliers causing increased costs. The workload of selected vendors can cause increasing prices and delay in delivery. If the Purchase Order documents are too voluminous or poorly structured or the Terms and Conditions or specifications too strict or not complete enough (e.g., no agreed conditions for variations), the vendor can suffer increased costs that he will try to pass along. Spare parts not identified at the time of purchase will not normally be competitively priced after the purchase order has been placed. If any purchasing or subcontracting constraints are imposed by project financing and are not properly accounted for in the estimate, costs can increase.

Finally, a favorite subject in managing costs – bulk materials. Bulk materials are generally purchased by providing bidders with take offs of the expected quantities and types. If the quantities used for selecting the vendor are not representative of the final requirements, even the most rigorous purchasing strategy may result in the wrong (not lowest cost) vendor being selected. If the types of materials given to the bidders are not inclusive of all requirements, the supplier may provide the additional types of materials at a non-competitive price.

5.7 CONSTRUCTION

Increased costs can be incurred during construction from a number of causes. The impacts of these increased costs can be passed along to the Owner, the General Contractor, or others depending on the contractual relationships. The Project Manager should be aware of the impacts and take the steps necessary to mitigate them.

Construction costs can increase by poorly qualified or experienced construction supervision, slow manpower mobilization, and delays in initial site work which can impact the succeeding construction activities such as underground piping, slabs, foundations, concrete structures, structural steel. Delays in delivery of drawings and materials can cause lower productivity, schedule delays, and rework. Poor shop inspection of fabricated equipment and materials can cause the field to have to rework the items or return them to the fabricator. Late modifications of construction documents or late recognition of pre-commissioning and commissioning requirements can cause rework and increase costs. Failure of subcontractors to perform as planned or financial failure of a subcontractor can lead to increased cost control issues and potentially large delays in construction performance.

5.8 JOINT VENTURE MANAGEMENT

Joint Ventures, either of Owners or Contractors can lead to cost over runs from a variety of causes. Managing the interfaces in a joint venture can become a full time job for the Project Manager and he may need to add staff to monitor and manage them. Having a well-qualified management team to assure technical coordination (choice of and compliance with rules, standards, and specifications), coordination of technical interfaces, and control of all joint venture expenditures, at time of their commitment, can make the joint venture a success.

Common sources of overruns in joint ventures are:

- Enforcing common methods in the joint venture rather than using each partner’s normal work processes and tools;

- Coding systems for common materials and documents implemented late or poorly;

- Split of responsibilities or services that are vague and/or unsuitable;

- Lack of motivating provisions for each company to keep their own costs under control and to keep from generating any increased costs for their partners; and

- Invoicing procedures to the joint venture being too complex and costly.

5.9 OTHER IMPORTANT POINTS

Other sources of cost control issues in project management include:

- Premature withdrawal of a key person from the project team with the resultant loss of knowledge and inertia; and

- Exchange rate risks.

5.10 CUMULATIVE IMPACT OF CHANGE

Change always causes increased project cost. But if project change becomes excessive, the “cumulative effect” of change can really add to the cost of the project – much more than the sum of the individual changes. Many studies show that the threshold for significant cumulative effect is about 10% of the contract price. When change exceeds 10%, in the aggregate, the ability of the project to evaluate and estimate the actual cost of each change is substantially diminished. Change gets overlaid with more change and costs tend to spiral out of control.

The Construction Industry Institute has done a lot of research on the cumulative impact of change. The following thoughts are from CII Research Publication 43-2 Quantitative Effects of Project Change:

- “Projects with a great amount of change experience lower-than-planned productivity.”

- At 25% construction change – construction productivity is about 7% lower.

- At 25% engineering change – construction productivity is 12% lower.

- At 25% engineering change – construction productivity is 10% lower.

- “Projects that start well and that are executed with little engineering change tend to run well in the field.”

- “Projects cannot endure numerous changes without suffering a decline in overall project cost performance.”

- “A Project Manager who may be experiencing a high degree of engineering rework and Client requests near the end of a project should seriously consider the impact of these changes on the main scope work. [Experience] would indicate that it may be advisable to defer discretionary changes until after the main scope of work is complete, if possible, or to assign a different crew to the change work. Even if the change is non-discretionary, it may be prudent to schedule implementation during periods when little other change work is anticipated.”

- “…construction projects are unique, one-time events. …Yet Project Managers often discount the early trends of a project, believing that time remains to recover schedule losses or negative trends.”

- “…projects that are trending late tend to finish late, and the ability to recover schedule declines with time, frequently due to an inability to resist ongoing changes.”

- “Very rarely do projects with early forecasts over budget actually come in under budget.”1

About the Author

Philip R. Moncrief, P.E., P.Eng., was a Senior Principal with Long International and retired in 2018. He has over 40 years of U.S. and international consulting experience involving engineering and construction, contract disputes, project management, project development, engineering/construction management, and process engineering. As an internationally recognized expert in the engineering and construction industry, he has managed large projects and had profit and loss responsibility for the engineering and construction operations of four major engineering-construction companies. He has published two books, has been a guest lecturer at the University of Colorado and Texas A&M University in their Construction Management Programs, and is a frequent presenter of project management topics to industry forums and seminars. For further information, please contact Long International’s corporate office at (303) 972-2443.

1 The Construction Industry Institute, Publication 42-3, Quantitative Effects of Project Change, Austin: Construction Industry Institute, 1995.

Copyright © 2004 Philip R. Moncrief

ADDITIONAL RESOURCES

Articles

Articles by our engineering and construction claims experts cover topics ranging from acceleration to why claims occur.

MORE

Blog

Discover industry insights on construction disputes and claims, project management, risk analysis, and more.

MORE

Publications

We are committed to sharing industry knowledge through publication of our books and presentations.

MORE