Developing Subcontract Pricing as Applied to Building Construction

INTRODUCTION

Cost and schedule control require cost engineers to have detailed knowledge and experience in the area of subcontractor construction cost evaluation. Subsequently the cost engineer will likely need a variety of resources for information that can be utilized to substantiate the basis and reasonableness of subcontractor cost data for use in various arenas of cost engineering. This paper provides general guidelines to commercial construction cost engineers for the development of a plan for obtaining and utilizing subcontractor cost information for use in bidding, procurement, scheduling, change order management, and claim management.

A discussion of the utilization of subcontractor’s cost examples and information from the beginning of estimate planning, bidding, and award of work, and continuing through the review and approval of costs for changes, and for the evaluation of potential additional cost claims is provided herein. The paper presents specific information that should be considered for the application of best practices and guidelines for use by contractors, cost engineers, and consultants.

The skills of any cost engineer can be enhanced by the practical utilization of subcontractor cost data throughout the various stages of project estimating, procurement, scheduling, cost claim preparation or evaluation, and maintaining historical cost information. Application of the procedures, methods, and information discussed herein should enable the cost engineer to achieve further knowledge and success through improved cost control throughout the various phases of the construction process.

In the area of commercial construction, cost engineers are involved with different responsibilities regarding the use of subcontractor cost data. The subcontractor firm itself will more than likely be engaged in estimating potential project costs, and ongoing project change orders. General contractor cost engineers often will be the recipient of proposal pricing from subcontractors as well as proposed change order pricing. Consultants are often utilized in the analysis of proposal cost and change order cost for the benefit of owners, contractors, subcontractors and other stakeholders requiring review, oversight, or analysis. Analysis of cost is required during the various phases of pre-construction, ongoing construction, and post construction activities. Forensic activities such as claims analysis for delay, disruption, impact or claims support are also areas requiring analysis of cost.

SUBCONTRACTOR COST DATA

Firms that are regularly engaged in the business of working as a subcontractor to provide services range from the very small company to the mega-corporation. Subsequently, the methods of estimating, maintaining historical cost information, and preparing change orders vary widely among these subcontractors. The cost engineer, however, will benefit from a complete understanding of the components of cost and the compiling of a historical database of actual cost for use with future estimates and change orders. The components of construction cost can be generally considered as labor cost, material cost, equipment cost, general project requirement cost, and overhead and profit cost.

As with any process, a plan must be developed to implement a historical cost database program. Obtaining cost data typically requires upper management to approve the plan for obtaining and compiling cost data and direct the implementation of the plan. Follow up inspection is also required to ensure proper documentation and gathering of information.

The construction pricing plan should typically include identifying the following:

- Create a data collection plan with emphasis on collecting current and relevant cost and risk data

- Establish parameters for the data that is to be gathered

- Identify the specific project types and conditions that should be used for tracking and establishing adjustment factors

- Investigate and identify data sources

- Establish a structure and coding system for the data

- Define the requirements of the person recording the raw data

- Determine the forms to be used in gathering the data

- Evaluate the use of technology in the process

- Determine the means and methods of cataloging the data

- Establish when and how the data is to be updated

- Collect data and standardize the identification of cost impact factors

- Baseline the data for benchmarking by adjustments and other impact factors

- Analyze the data for cost drivers, trends, and outliers

- Compare results against rules of thumb and standard factors derived from historical data

- Interview data sources and document all pertinent information

- Store data for future use

Developing the database requires a practical approach to defining the parameters for the activities and components of construction that are to be tracked for labor and material cost data. The parameter chosen is typically defined as the identification of significant activities and components that are readily measurable and characterize the system or variable to be measured. Each item, activity, or component must be then defined in a unit of measurable quantity that can be related to labor and material cost. The cost must then be identified. Whether cost data is obtained from self-performed work in place or other sources such as actual bids, cost guides, or projects built by others, it is important to be clear about what the costs include and do not include. If the data is obtained from self-performed work, then the task of defining cost in most cases should be fairly straight forward. In general terms, actual construction cost can be separated into the following categories:

- Direct field labor cost

- Indirect labor cost: labor taxes, health and welfare, workman’s compensation, FUI, SUI, FICA, and other direct payroll costs such as dues, insurances, profit sharing, etc.

- Direct consumed material cost

- Direct small tools cost

- Direct cost of material installed as required by the contract documents for construction

- Indirect onsite overhead and cost of operations such as requirements needed for: general contingencies, bonding, insurance, permits, fees, management personnel, site office, material storage, material protection, personnel access, communication, security, hoisting, scaffolding, weather protection, quality control, life safety, survey, transportation, utilities, inspection, testing, design, etc.

- Indirect general office overhead cost including requirements for the ongoing and continued operations of the company such as: upper management personnel, administrative, legal, marketing, financing, association, research, planning, development, etc.

- Profit

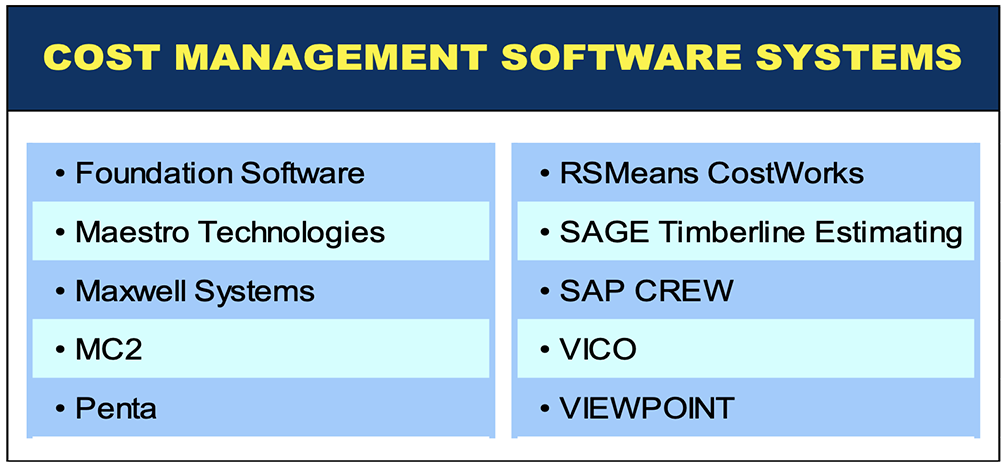

There are a number of existing established cost management software systems and structures that have already identified the parameters of cost breakdown for measurement and identification of items and components of work on which data can be compiled. Many of the systems available for use provide industry wide statistical production rates as well as the identification of components that define what costs are included for each item to be installed and thus provide general guidelines for information to be gathered when developing a cost database plan. Some of the software resources available include:

Table 1: Cost Management Software Systems

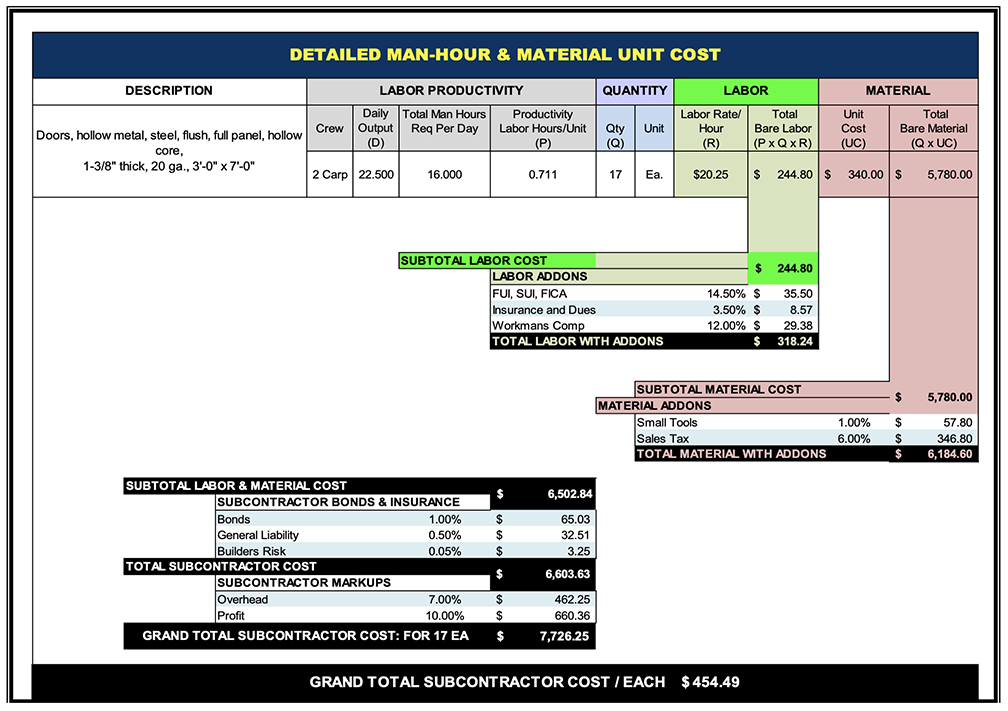

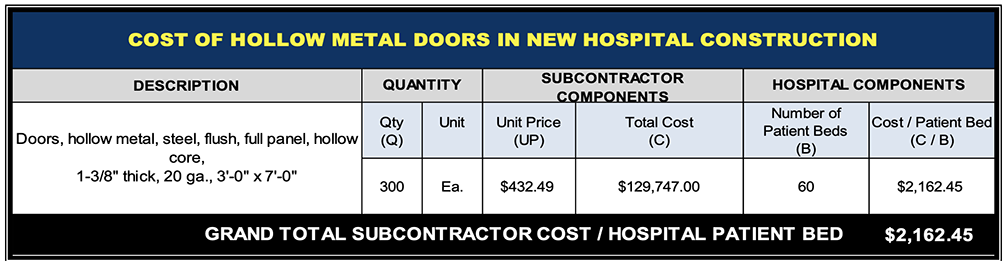

Once the raw data is obtained, the information can be reviewed for logic and reasonableness. One of the most important quantities of measure is the number of man hours required to accomplish the installation of a task which is also known as productivity. A major goal of the development of a cost database is to establish the baseline of productivity. Establishing this baseline results in the identification of the factors to use for adjustment of the baseline to the specific and various conditions in which the work was or is to be performed. As the data is compiled, different levels of detail can be established. The different levels of detail provide the user with information that can be used as unit cost data, square foot (or square meter) data, assembly cost-data, and systems cost-data. Examples of some of the levels of detail that can be established are shown in the following tables.

Table 2: Detailed Man-Hour & Material Cost per Unit

Table 3: Cost per Square Foot of Hospital Building Area

Table 4: Cost per Hospital Bed

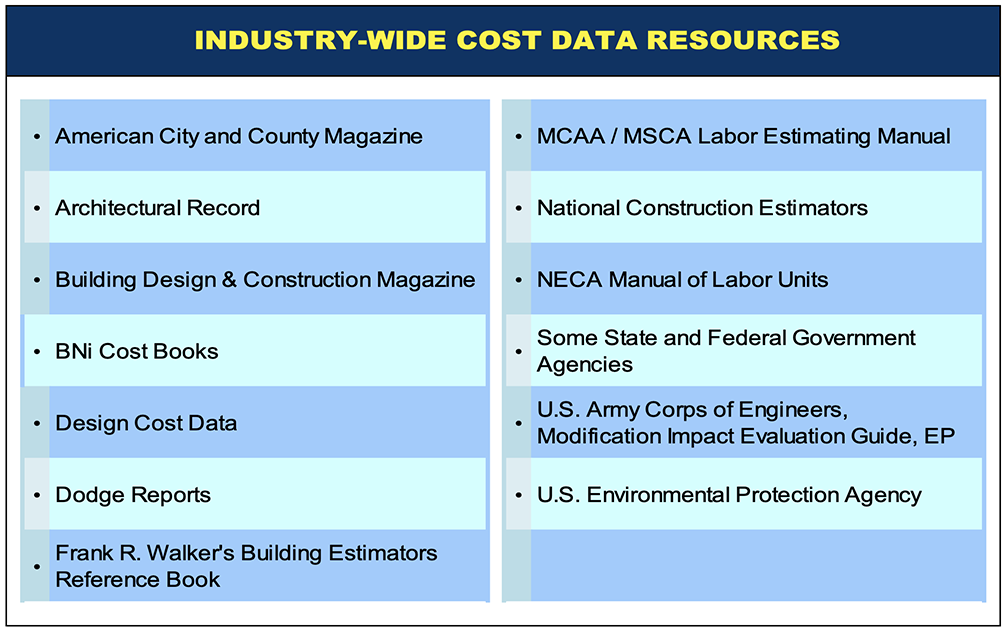

There are a number of existing established resources that provide cost data in various forms of detail, including detailed man hour production, unit cost data, square foot (meter) data, assembly cost data, and systems cost data. Many of these resources provide industry wide statistical cost information, as well as the identification of differentiation types that can also be used as general guidelines for compiling information. Some of the resources available include:

Table 5: Industry-Wide Cost Data Resources

There are numerous publications regarding man-hour production rates and cost information. The list above is not meant to be comprehensive. The list is only a partial representation of the many other professional and trade publication resources available.

THE NON-SUBCONTRACTOR

Firms that are not working as a subcontractor, but who use the services of subcontractors or only rely upon the cost information provided by subcontractors, comprise a variety of firms and industries. Subsequently, the importance and ability to determine the reasonableness of the cost can significantly impact the user’s financial success. The user will generally have to rely upon comparative data to accurately assess the estimate, bid, change order or proposal. Obtaining and/or maintaining historical and up to date cost information will benefit the user of the subcontractors’ services and information. Analysis of cost requires a thorough understanding of the components of cost and the factors that may impact the cost data used to assess the subcontractors’ cost. The importance of understanding the components of construction cost is paramount to successful analyses cost. Again, the components of cost are generally considered to be labor cost, material cost, equipment cost, general project condition cost, and overhead and profit cost.

Obtaining data for testing or assessing subcontractor cost requires awareness of where the information is available. Subcontractors routinely provide cost data to others as a normal part of their interface with clients. Typical first hand sources for present and past cost data are identified as follows:

- Concurrent bidder’s pricing information

- Unit prices provided by bidders

- Cost information provided for loading schedules

- Payment Request breakdowns

- Cost information used to support Cost Plus work

- Cost information used to support Change Orders

Secondary sources for cost data include but are not limited to those sources listed previously in both Table 1 and Table 5.

The costs of materials are more easily obtained than the costs of labor or installation. Material pricing can be obtained from the vendors or suppliers and distributors of the same. In many circumstances, distributors and suppliers will provide quotes or confirm pricing to those wishing to obtain cost information. Relationships formed with vendors can prove to be an invaluable resource to cost engineers for establishing cost data. Similarly, relationships made directly with subcontractors can also prove to be beneficial to the cost engineer.

A plan must be developed to implement a historical cost database program. Obtaining cost data typically requires upper management to approve the plan for obtaining and compiling cost data and then directing the implementation of the plan. Follow up inspection is also required to ensure proper documentation and gathering of information.

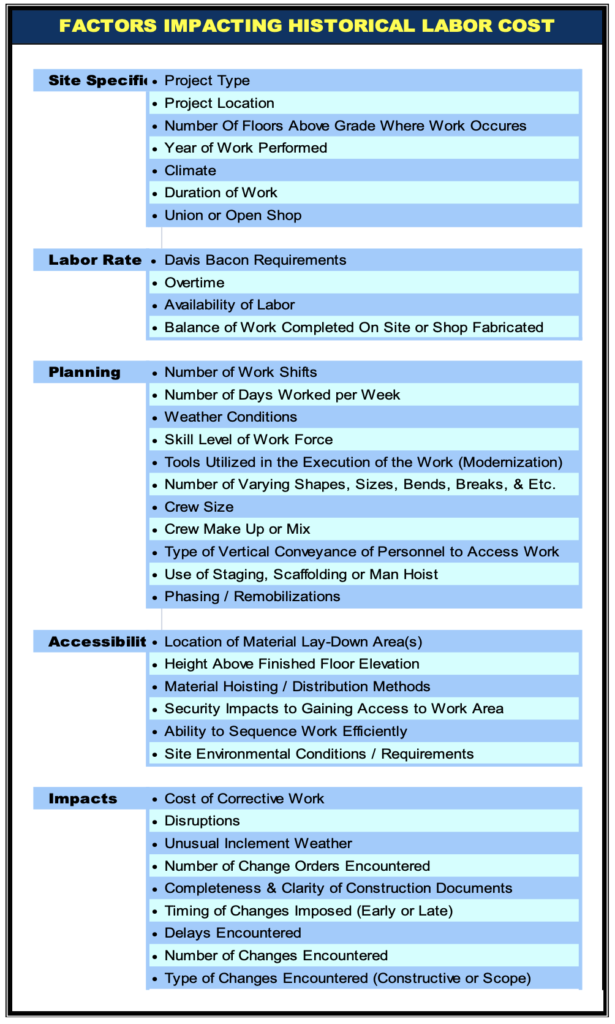

When compiling cost data and generating a historical cost database, the cost engineer must consider the numerous factors which impact the cost of material and installation. The following is a list of the factors that impact historical labor cost. The factors include Site Specific, Labor Rate, Planning, Accessibility, and Impact categories.

Table 6: Factors Impacting Historical Labor Cost

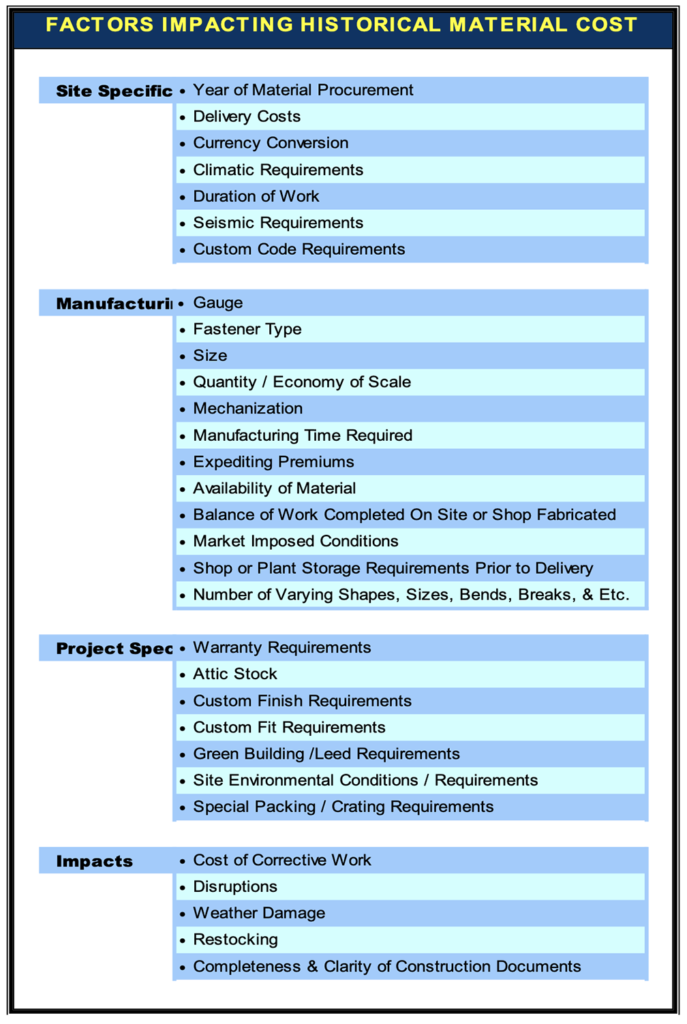

Although not as numerous, there are many variables that impact material costs. The following table identifies many of the variables that should be considered when building a database of material cost information.

Table 7: Factors Impacting Historical Material Cost

Most of the cost data that is available regarding subcontractor cost is not clearly defined regarding material and labor factors that affect such costs as those listed in the previous tables. However, the factors listed herein should be considered in composing historical cost. The most common parameters used regarding subcontractor costs are project location, union or non-union, year of work performed, height above finish floor, and project type. Expertise in the cost of subcontractor work is achieved through continuous understanding, awareness, and collection of information which vary the cost of work.

Although not specifically addressed, in the above list of factors impacting cost, other factors such as the size of the firm, size of project, amount of risk, and competitiveness should also be considered in collecting cost data.

SUBCONTRACTOR COST DATA UTILIZATION

The advantages of having quality subcontractor cost data are significant. The cost engineer can utilize the factors affecting cost to adjust historical cost data to reasonably evaluate subcontractor data. The cost engineer can then compose target estimates to compare against actual bids or in the negotiation of subcontracts. Cost loading of schedules can be measured against historical cost metrics. Change order costs are more readily understood. Disputes regarding costs are more likely to be resolved without actual claims being filed.

In the preparation of schedules, manpower levels, durations and cost loading information should be derived from the estimate. The application of correctly loaded information enhances the ability of stakeholders to use the schedule for accurate cash flow projections and assessment of progress payment requests. Variations can be studied to determine potential delays to the work or to determine alternate sequences. Manpower projections, phasing interfaces, and other capabilities are available. Cost engineers who are experienced and knowledgeable of historical cost information are better equipped to analyze productivity.

RECOMMENDED GUIDELINES

Cost engineers are encouraged to maintain awareness and knowledge of the variables that influence cost of work put in place by subcontractors. For the contractor, profit and loss can be assessed by the cost engineer who has up-to-date cost information. The reasonableness of subcontractor pricing that will be potentially used in bids or proposals can assist in resolving concerns prior to bid versus wishful thinking or bad faith use of bids.

Requesting unit pricing and specific breakdown of pricing from subcontractors is warranted where cost control is desired by builders, developers, and owners. Subcontractors and vendors are generally more receptive to providing detailed cost information prior to award of work than they will be willing to after the work is awarded. Whenever possible, cost engineers engaged in receiving and preparing cost proposals should request the following information prior to award:

- Crew mix breakdown

- Pay rates by labor classification

- Breakdown and identification of labor markups and add-ons

- Number of manpower required

- Number of and level of supervisors

- Unit prices for added or deducted work

- Unit prices for added or deducted material

A detailed schedule of values will typically be a requirement in the contract documents. The detailed schedule of values provides an opportunity to obtain useful cost data. The following is a recommended breakdown of the general category descriptions that should be used in the schedule of values for each subcontracted discipline of work. The breakdown can be modified for specific use with a variety of subcontract work descriptions and disciplines. When appropriate the breakdown can also be broken down as needed by area, sector, process, system or other component needed to more thoroughly address the additional needs of stakeholders. The schedule of values breakdown may include the following categories:

- Mobilization

- On Site General Requirements by: Material, Labor & Equipment

- Permits & Fees

- General Overhead & Profit

- Major Material & Equipment

- Systems by: Material, Labor, Rough In, Fit Out, Finish or Trim Out

- Punch Out by: Material, Labor

- Start Up Costs by: Material, Labor

- Testing Costs by: Material, Labor

- Demobilization

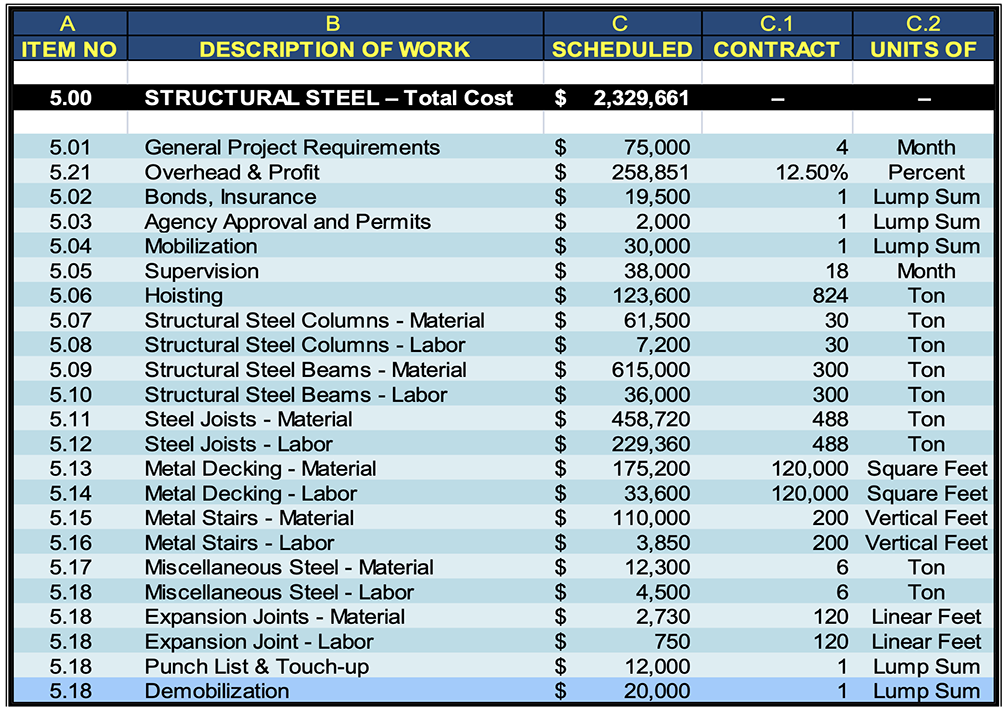

The cost engineer should bear in mind that the schedule of values typically submitted is not a detailed listing of the work to be performed, but is a list of work items that should identify enough components of a project to determine progress and maintain the enforceability of surety bonds or the equivalent through scrutiny of the work put in place and the value thereof. The following is a simplified example of a schedule of values for a structural and miscellaneous steel subcontract.

Table 8: Sample Schedule of Values for a Structural Steel Subcontract

CONCLUSION

The collection and structuring of historical cost data that can be adequately adjusted to the specifics of any given project is imperative to the development of representative, probable and reasonable project specific cost information. With knowledge and experience, the cost engineer utilizing the well-defined database of subcontractor cost data will be able to adjust the costs for impacting factors in order to formulate more accurate, valid, consistent, and comparable estimates, change orders and scheduling. This approach allows for previously developed estimates and cost information to be adapted to a system of reporting, documenting, and supplying of information to substantiate and validate the basis of cost information. As the cost engineer proceeds through the process of determining adjustment factors to be applied to the cost database, the identification of uncertainties that impact cost will become easier to understand and identify.

The process for developing credible construction pricing, cost models, estimates, target estimates, change orders, and scheduling will be greatly enhanced by providing a resource of data and detailed information that is based upon proven and reliable information.

The knowledge gained in continuous work with the compiling and adjusting of subcontractor pricing and cost data can overcome challenges that face cost engineers by providing an available source of reliable historical data that has been normalized and can be adjusted to specific project needs. Practice in the use of the information should result in realistic assumptions and reasonable cost information that leads to reducing over-optimism and unrealistic projected costs or savings from the beginning of estimate planning, bidding, and award of work and continuing through the review and approval of costs for changes. Cost engineers who evaluate and analyze cost and scheduling information prepared by others will also be able to provide stakeholders with a better understanding and ability to judge the reasonableness of the information being evaluated.

About the Author

John E. Cheek, CPE, was a Senior Executive Consultant with Long International and has over 40 years of professional experience gained in cost engineering, scheduling, bidding, planning, contracting, and claim analyses in commercial and industrial construction. He is an expert in the evaluation of construction cost claims, schedule impact delay analysis, arbitration/mediation support, and dispute resolution. He has been involved with numerous commercial, institutional, and industrial projects nationwide. Mr. Cheek’s claims and litigation support services include testimony in arbitration and mediation and assisting corporations, municipalities, developers, contractors, and insurers. His involvement has included government projects, resorts, hotels, schools, condominiums, retail facilities, and industrial projects. He has prepared more than twenty cost estimate analyses, written expert report supplements and evaluations, and supported attorneys in depositions, mediations, and settlement negotiations. Mr. Cheek earned a degree in Civil Engineering Technology, Surveying, and Construction from Southern Technical Institute in 1978. For further information, please contact Long International’s corporate office at (303) 972-2443.

Originally published by AACE International as CSC.S04 in the 2010 AACE International Transactions.

Reprinted with the permission of AACE International, 1265 Suncrest Towne Centre Dr., Morgantown, WV 26505 U.S.A.

Telephone: +1 (304) 296-8444 | Facsimile: +1 (304) 291-5728 | web.aacei.org | Email: info@aacei.org

Copyright © 2010 by AACE International; all rights reserved.

ADDITIONAL RESOURCES

Articles

Articles by our engineering and construction claims experts cover topics ranging from acceleration to why claims occur.

MORE

Blog

Discover industry insights on construction disputes and claims, project management, risk analysis, and more.

MORE

Publications

We are committed to sharing industry knowledge through publication of our books and presentations.

MORE