April 7, 2025

Discrete Damages/Cost Variance Analysis Method for Calculating and Presenting Damages in a Construction Claim

When a contractor’s costs exceed its contract amount on a construction project due to owner-caused impacts, the contractor can choose from several damages methods in seeking equitable compensation.

If the claimant can show 1) entitlement to recover for the other party’s wrongful conduct, and 2) damage incurred because of that wrongful conduct, the claimant may recover even though the amount of the damage is uncertain or is based on estimates. There are several methods currently in use for the calculation of recoverable damages.

Previous blog posts address the Total Cost, Modified Total Cost, and Jury Verdict methods, as well as Quantum Meruit and the A/B Estimate and Delta Estimate methods. This post will briefly discuss the Discrete Damages/Cost Variance Analysis method. For more detail on the steps involved with this method, see the article Discrete Damages and Cost Variance Analysis Method for Quantifying Damages in Construction Claims.

The Discrete Damages/Cost Variance Analysis method is a variation of the Delta Estimate and Modified Total Cost methods and allows claimants to go a step further in providing convincing proof of damages incurred.

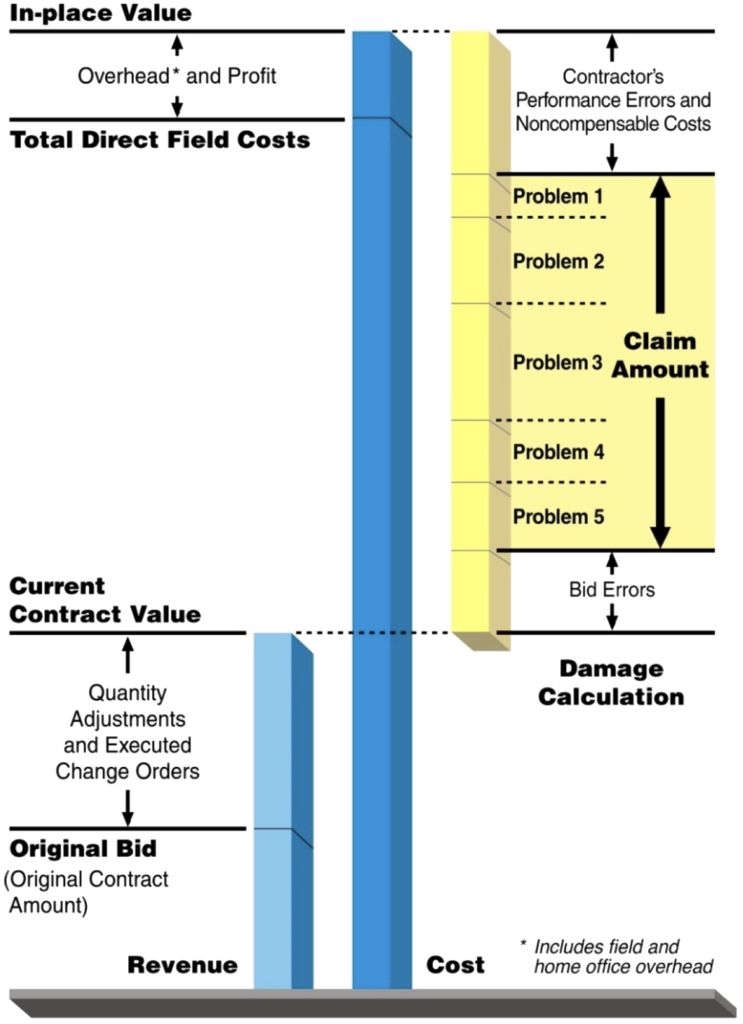

With this method, the analyst distributes all costs incurred on the project rather than quantifying only the claimed costs, as may be done in the other methods. The analyst establishes credibility by differentiating cost increases that result from bid error, noncompensable problems, and compensable problems and then tying specific costs to each compensable problem. In addition, the analyst applies the cost growth for each discrete claim to each relevant cost account (or group of accounts) to demonstrate that the “sum of the parts” of each claim does not exceed the entire cost overrun for each cost account. Figure 1 illustrates the Discrete Damages/Cost Variance Analysis method:

Figure 1: Discrete Damages/Cost Variance Analysis Method

In addition to evaluating cost growth for each cost account (or group of accounts), the analyst may consider quantity, man-hour, unit price, and unit productivity variances for each account based on a comparison of the current budget and actual values for these indices, to the extent that such data is available. Because of the comprehensive nature of this type of analysis, it relies heavily on the contractor’s contemporaneous detailed man-hour and cost records and reports, and the current budget versus actual quantity, man-hour, and cost data derived for each account.

The analyst distributes all costs taken from the claimant’s cost records into Cost Variance Analysis categories, which include the original bid, any bid errors, approved changes, pending changes, specific compensable problems (claims), and noncompensable (or unrequested) costs. Because the claimant assigns a particular item of damage to each compensable problem, calculating the costs establishes the cause-effect relationship. Thus, the claimed amount is both easy to verify and difficult to refute. Most contractors maintain cost records that have some degree of subdivided cost account detail. Credibility is increased by demonstrating variances at the greatest level of detail possible using the available cost records.

The analyst may employ varying types of analyses and cost apportionments when there are several interrelated problems, such as when numerous owner-caused changes as well as contractor-caused bid errors and performance problems impact a project.

For example, assume that a contractor has experienced a cost overrun of $100,000 across four separate cost accounts associated with piping labor. In one analysis, the contractor quantifies a bid error of $10,000 related to missing scope of work. In a second analysis, the contractor determines that disputed change order requests include $15,000 of piping labor. In a third analysis, the contractor uses industry studies to quantify $50,000 of direct piping labor disruption associated with overtime and overcrowding. In a fourth analysis, the contractor quantifies $5,000 of increased piping labor costs due to overtime labor rate premiums. Of the $100,000 lost, the contractor has accounted for $80,000, of which $70,000 will be claimed. If the extent of project change was significant enough to support a cumulative impact claim, some or all the residual $20,000 in these accounts could be claimed. If not, the contractor could still demonstrate that it is not claiming more than it lost.

This method may be difficult to apply in a case where there are several interrelated problems, but any attempt to segregate and price claims separately will generally increase the chance of recovery. Because of the detailed analyses involved, this method can be more time consuming and costly to prepare than other methods, and it can only be implemented if the contractor has maintained detailed cost and man-hour records.

The advantages of the Discrete Damages/Cost Variance Analysis method are as follows:

- Because all components of the cost records are evaluated and distributed into the claim matrix, the total value of the requested funds can be fully explained and justified.

- The link between entitlement and the amount of damages is developed at the lowest level of detail of the cost records, thus providing significant credibility to the burden of proof.

- Isolation of the damages cost components and individual claim problems identifies hard areas of claim as well as soft spots to be negotiated, if necessary.

ADDITIONAL RESOURCES

Blog

Discover industry insights on construction disputes and claims, project management, risk analysis, and more.

MORE

Articles

Articles by our engineering and construction claims experts cover topics ranging from acceleration to why claims occur.

MORE

Publications

We are committed to sharing industry knowledge through publication of our books and presentations.

MORE

RECOMMENDED READS

Methods for Calculating and Presenting Damages in a Construction Claim

This blog post describes seven methods for calculating and presenting damages in a construction claim and how to choose one.

READ

Total Cost Method for Calculating and Presenting Damages in a Construction Claim: Part 1

This blog post discusses the Total Cost method, including elements of proof, theoretical bases, and prerequisites.

READ

Total Cost Method for Calculating and Presenting Damages in a Construction Claim: Part 2

This post addresses topics related to the Total Cost method, including the Total Cost cumulative impact claim.

READ